How Banks Stop Losing Business Customers to Fintechs

For years, the business banking relationship was anchored by the business checking account. Today, that anchor has come loose. As fintechs capture a growing and significant share of the B2B card market, banks are realizing that business customers no longer want a place to store money. They want tools that actively help them run their business.

The question facing every bank leader is the same: do you watch the migration happen, or do you build something that stops it? The answer lies in how banks think about their card programs. Not as a commodity product, but as a modern card and spend program that deepens client relationships and keeps wallet share in-house.

Unlike fintechs which compete directly for interchange and clients, Pliant takes the opposite position. It is a technology partner that delivers fintech-grade card and spend capabilities under the bank's own brand, strengthening the commercial offering while keeping the customer relationship with the bank.

In this article, we cover the key strategies banks are using to defend and grow their business relationships. We cover:

How legacy vs. modern card programs drive top-of-wallet status

How banks can launch a competitive program without rebuilding their core

How modern programs reduce bank cost-to-serve

Legacy vs. Modern Card Programs: What Actually Drives Top-of-Wallet Status

"Top of wallet" means being the card a business reaches for first. The one employees use by default for company spending. Today, that status is not won by brand recognition or reward points. It is won by the issuance speed and spend controls a modern card program delivers.

Banks on legacy card stacks often require manual steps to adjust limits, issue cards, and restrict spend by category. Modern platforms can do much of this in real time through web and mobile experiences. That difference in experience determines which card gets used for every transaction.

The numbers reflect this. Banks using modern card platform partners consistently report significantly higher card utilization compared to those on legacy stacks, simply because the cards are easier to deploy and control. Higher utilization means more interchange revenue, more data, and a stronger day-to-day presence in the client relationship.

The control layer matters just as much as the issuance speed. Modern platforms allow granular configuration: a card issued for "Software Subscriptions only," a team budget with real-time alerts, a single-use card for a supplier payment. Each of these controls creates a usage habit that deepens the relationship. Legacy systems cannot replicate this, and businesses that discover the difference rarely go back.

From Payment Product to Relationship Platform: Why Customers Stay

The reason businesses switch to fintechs is not just that fintechs have better cards. It is that fintechs have built something businesses use every day. The card is the entry point. What keeps a business on a fintech platform is daily engagement: instant card issuance, built-in spend controls, automated expense management, AP flows that run without manual effort. Every interaction makes the product more embedded, and a more embedded product is harder to leave.

Banks that deliver a modern card and spend program gain the same dynamic, under their own brand, without giving up the client relationship.

Three things change when a bank moves from a legacy card product to a modern program:

Daily engagement replaces monthly statements

Instead of a business checking its card statement once a month, the platform becomes a tool finance teams use every day. That visibility creates reliance, and reliance creates retention.

Card usage increases significantly

Banks that offer modern, easy-to-deploy card programs consistently see higher card spend per client. Higher usage means the bank is deeper in the customer’s spending life, not on the periphery.

The client relationship stays with the bank

Pliant's white-label model means the bank's brand is what customers see. There is no customer disintermediation. The bank keeps the relationship, the data, and the cross-sell opportunity.

This is the core counter to the fintech threat. Fintechs win by becoming the default tool. Banks that launch a modern card and spend program reclaim that position. And because they already have the trust and the broader relationship, they are harder to displace once they close the product gap.

Pliant's Card & Spend OS is purpose-built for banks to launch a fully branded, next-generation card program. Explore Card & Spend OS.

How Banks Can Launch a Competitive Card Program Without Rebuilding Their Core

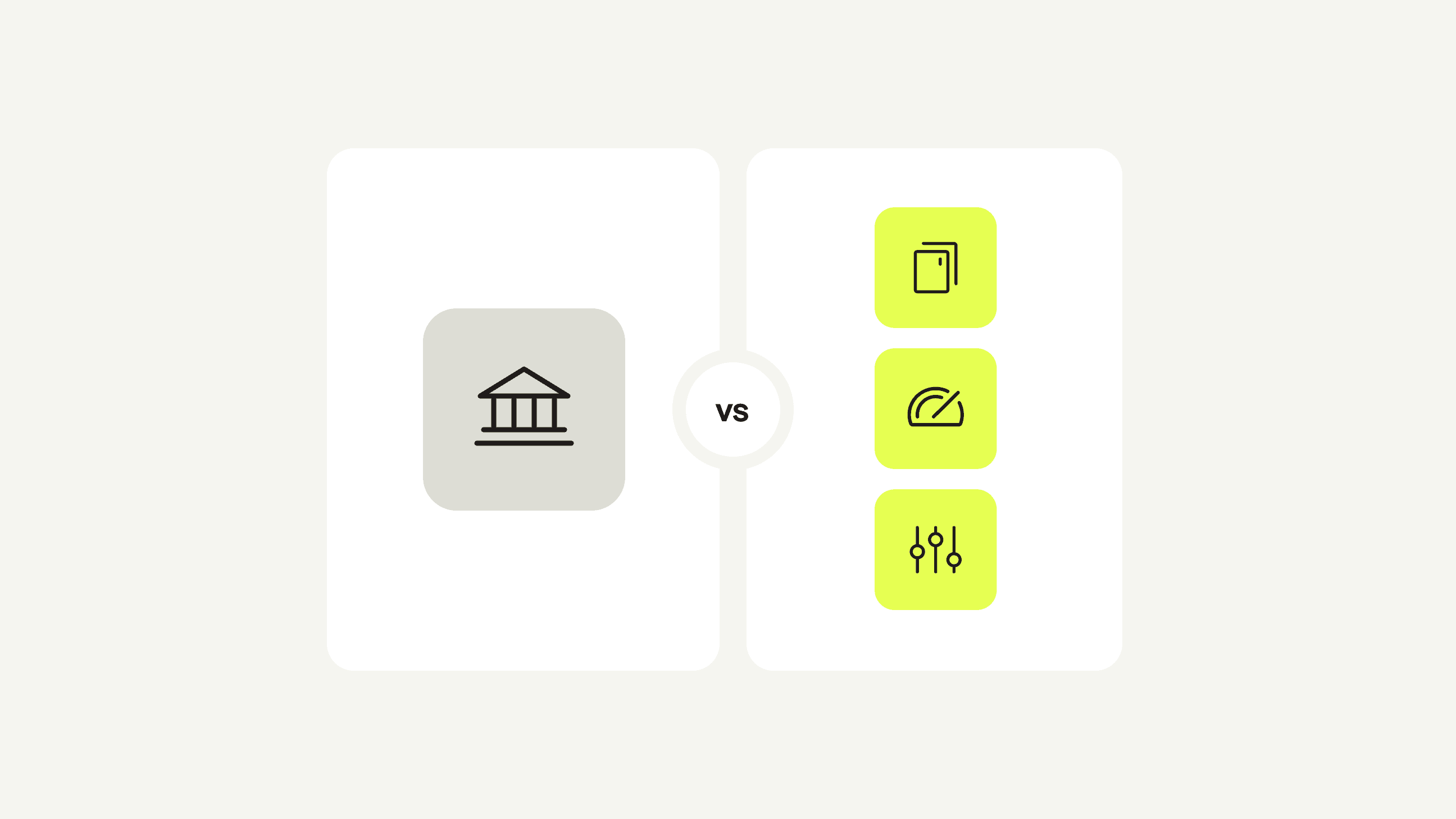

One of the most common objections from bank executives is that modernizing the card program requires a multi-year transformation project. It does not. The architecture is modular. Banks do not have to choose between speed and control.

The goal is not only speed. It is speed while keeping the customer relationship with the bank, leveraging existing systems where needed, and relying on a partner to cover complexity in the background.

Pliant's modular bank partnership architecture is built around a set of independent services: Transaction, Settlement, Card, Payment, Organization, Billing, and Integration. These connect to a bank's existing infrastructure or be fully provided by Pliant. The bank does not replace its core. It connects at the layers it chooses and leaves the rest untouched.

The depth of integration determines time to go-live:

BIN Sponsorship: Pliant provides the issuing license, onboarding, risk management, and credit lines. The bank launches a fully branded card program with web and mobile apps under its own design, with no development effort required on its side.

BYO License: The bank uses its own issuing license, existing processor, and regulatory framework. Pliant integrates into that infrastructure, delivering the same fintech-grade experience under the bank's brand. More control, deeper integration.

Intermediate configurations are also possible, allowing banks to start at the faster entry point and expand integration depth over time as the program scales.

Banks do not need to rebuild everything to defend share. They need to choose the right integration model for their situation and launch before a fintech or a better-equipped bank does it first.

Ready to build a card program that keeps business customers?

Pliant is the technology partner that helps banks deliver what fintechs offer. Explore how Pliant's Card & Spend OS helps banks launch modern, fully branded B2B card programs at fintech speed.